Isso já foi algo que apareceu no final do ano passado, nunca ninguém entendeu o que era aquilo, porque acho que nunca apareceu em nenhum leak

Atom? Com esse nº de pins?

Atom? Com esse nº de pins?

O tweet acertou que o SPR irá ter SKUs com HBM, mas algo com mais de 7500 pins a usar Atoms? A única coisa de grandes dimensões que existiu no passado a usar Atoms foram os Xeons Phi e a partir do momento que a Intel está a apostar em GPUs mais tradicionais, não me parece que vão por aí.Atom? Com esse nº de pins?

Que raio......Little Cores num Socket gigantesco não era algo que esperasse da Intel nos próximos tempos. É verdade que depende do que foi "Modified" nos Atoms, mas custa-me a ver qual é a perspectiva e o mercado alvo que a Intel tem para esse produto. Little Cores para o mercado Servidor não teve grande sucesso e não estou a ver a Intel a fazer renascer os Xeons Phi, especialmente em Socket, depois de começar a apostar em GPUs tradicionais.Mas agora voltou tudo, com o Moore's Law e o Adored...

Why has Intel fallen behind TSMC and SEC in semiconductor fabrication, and why is it unlikely to catch up? The problem is that Intel is engaged in two types of competition, one with companies like TSMC and SEC in cutting-edge fabrication technology and the other within Intel itself between innovation and financialization.

The root of Intel’s failure in organizational integration lies in the financialized character of a third social condition of innovative enterprise, strategic control. Accepting stock yield as the measure of enterprise performance, in recent years Intel’s senior executives who exercise strategic control have lacked both the incentive and, increasingly we would argue, the ability, to implement innovative investment strategies through organizational integration.

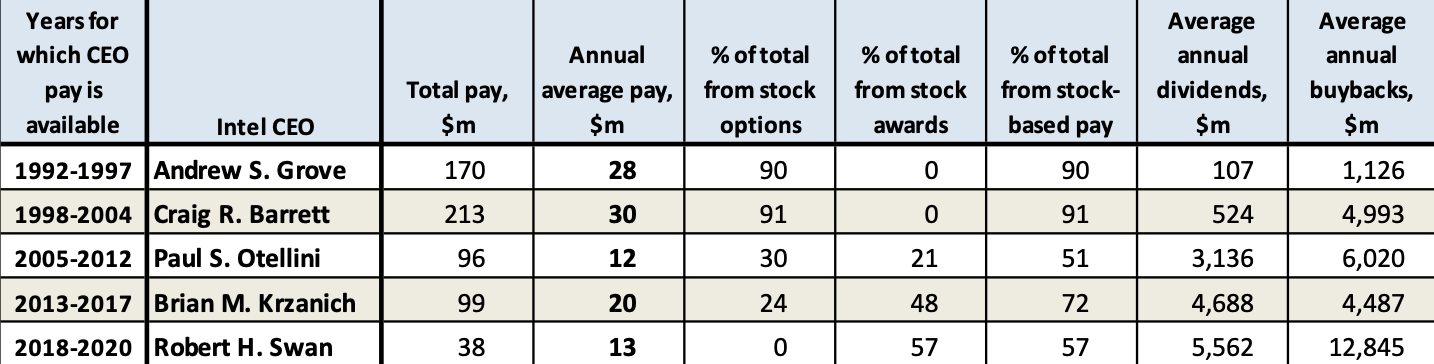

Executive stock-based pay, in the form of stock options and stock awards, has created incentives for Intel’s CEOs to do large-scale buybacks to give manipulative boosts to the company’s stock price. Table 3 documents the total compensation, including realized gains from stock options and stock awards, of Intel’s CEOs over the past three decades.

In an interview broadcast by CBS’s Sixty Minutes on May 2, Gelsinger complained that the U.S. share of world semiconductor manufacturing had declined from 37% to 12% in the past 25 years and told interviewer Lesley Stahl that “Intel has been lobbying the U.S. government to help revive chip manufacturing at home—with incentives, subsidies, and-or tax breaks, the way the governments of Taiwan, Singapore, and Israel have done. The White House is responding, proposing $50 billion for the semiconductor industry in the U.S. as part of President Biden’s infrastructure plan.”

Stahl asked Gelsinger why, given its profitability, Intel needed U.S. government support, to which the CEO invoked U.S. national interest: “This is a big, critical industry and we want more of it on American soil: the jobs that we want in America, the control of our long term technology future, and as we’ve also said, the disruptions in the supply chain.”

https://www.ineteconomics.org/persp...-lost-leadership-in-semiconductor-fabricationStahl countered: “You have spent much more in stock buybacks than you have in research and development. A lot more” (for the record, in 2019-2020, Intel spent $27.8b. on buybacks and $26.9b. on R&D). Gelsinger replied: “We will not be anywhere near as focused on buybacks going forward as we have in the past. And that’s been reviewed as part of my coming into the company, agreed upon with the board of directors.”

https://www.tomshardware.com/news/i...tm_source=twitter.com&utm_campaign=socialflowAccording to a report from the Wall Street Journal citing people familiar with the matter, Intel is in talks to buy GlobalFoundries for roughly $30 billion.

É a intel que vai fazer os IO dies para os cpu's da AMD?Como é que coisa destas poderá passar pelos reguladores...

Isso é "ultrapassável". Depende de cliente para cliente, depende dos preços, depende das garantias, etc.Isto se a politica da Intel não mudar radicalmente. E mesmo que mude, é difícil que seja alternativa real visto que os potenciais grandes clientes (AMD, Apple, Nvidia e até Qualcomm) são concorrentes directos da Intel.

Uma compra da GF por parte da Intel, pode ser algo mais complexo e envolver mais partes do que parece. Se olharmos para o mercado e se for só nessa perspectiva, de facto, 5% de quota não é muito.A haver esta compra a GF pode investir em novos processos, evoluir os que tem e ganhar mais alguns clientes, mas ser concorrente a sério da TSMC não chega lá certamente.

Intel said in its filing that in the final quarter of 2021 it would be taking a $300 million writeoff for its Intel Federal business, which we strongly suspect is some kind of charge relating to the ill-fated “Aurora” exascale supercomputer that is based on Sapphire Rapids processors and “Ponte Vecchio” Xe HPC GPU accelerators that is being built by Intel and Hewlett Packard Enterprise for Argonne National Laboratory.

https://www.nextplatform.com/2021/07/22/its-all-uphill-from-here-for-intels-datacenter-business/Intel didn’t say that, but we suspect that is what it is, and if it is, and Intel and HPE/Cray are still building the system, which had a price tag of over $500 million with $100 million of that going to Cray (which won the deal with Intel before HPE bought the supercomputer maker). Intel may be writing off a chunk of the Argonne contract as a loss and also rolling up a slew of HPC stuff into the carpet before it stuffs it in the trunk of a 1970 Cadillac colored the same as the Intel Inside logo.

This means that the limit of the first generation Foveros which needed a top die smaller than the base die is now removed. The top die can be larger than the base die, or if there are multiple die on each of the levels, they can be connected to any number of other silicon. The goal of Foveros Omni is really to solve the power problem as discussed in the initial section on Foveros – because power carrying TSVs cause a lot of localized interference in signaling, the ideal place to put them would be on the outside of the base die.

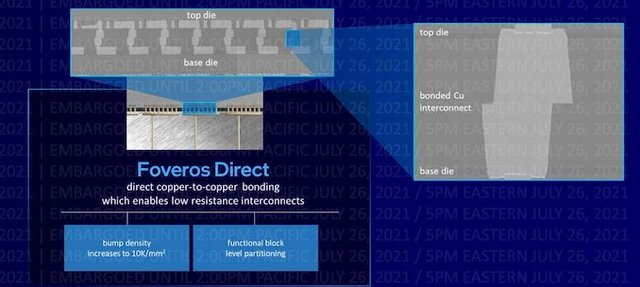

https://www.anandtech.com/show/1682...nm-3nm-20a-18a-packaging-foundry-emib-foverosFoveros Direct is a technology that helps Intel drive the bump pitch of its die-to-die connections down to 10 micron, a 6x increase in density over Foveros Omni. By enabling flat copper-to-copper connections, bump density is increased, and the use of an all-copper connection means a low resistance connection and power consumption is reduced. Intel has suggested that with Direct, functional die partitioning also becomes easier, and functional blocks could be split across multiple levels as needed.

Technically Foveros Direct as a die-to-die bonding could be considered complimentary to Foveros Omni with the power connections outside the base die – both could be used independently of each other. Direct bonding would make internal power connections easier, but there would still be the issue of interference perhaps, which Omni would take care of.

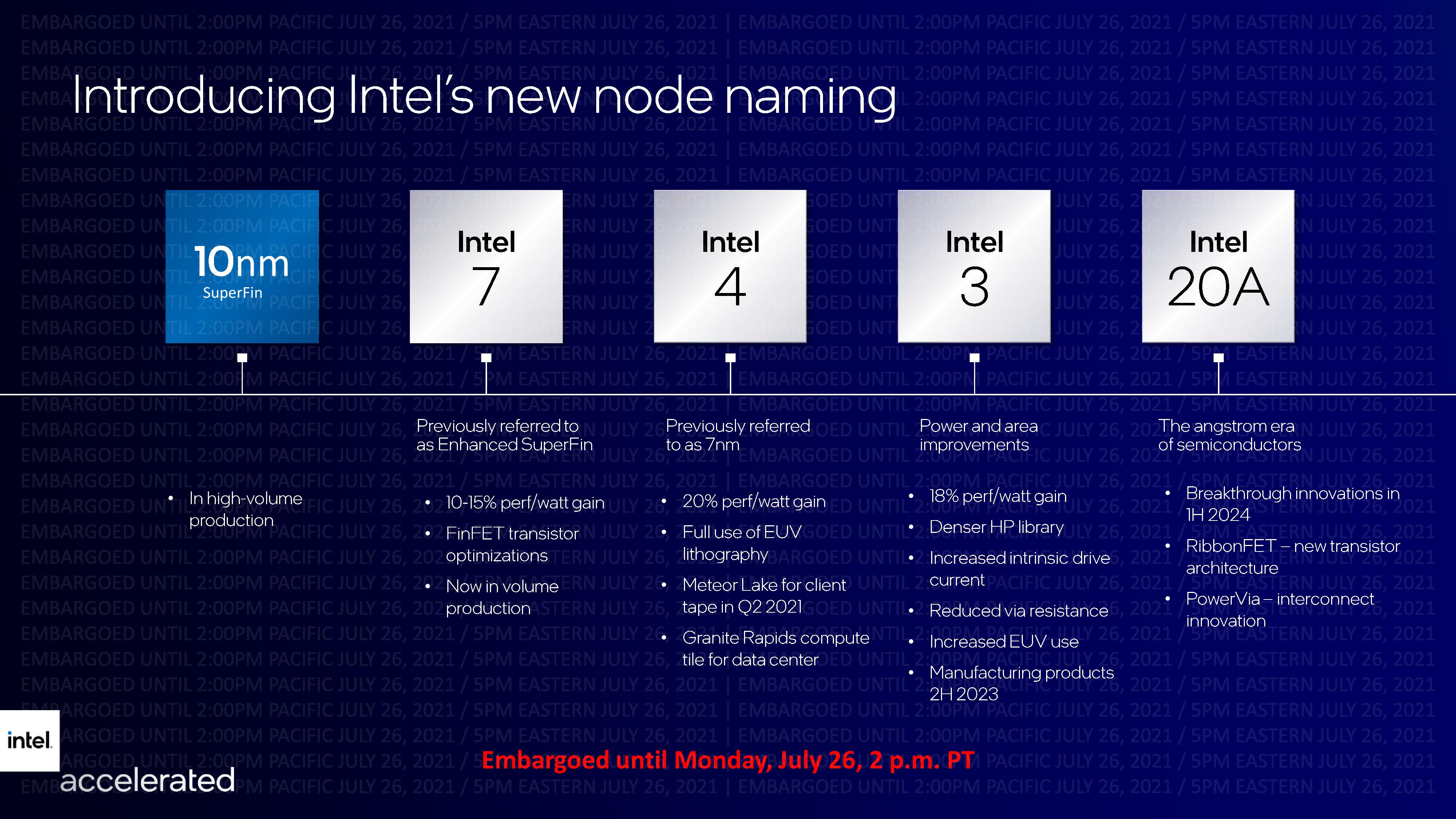

While you can read the text in the chart above, there are a few items we wanted to point out. First, we have the “Granite Rapids compute tile” for a future Xeon. Intel is fully embracing the “glued together” CPU methodology and that is why we have a compute tile in Intel 4. Meteor Lake will also be on Intel 4. Intel 3 is slated for 2023 which likely means volume products in 2024 if that schedule holds since there is typically a lag between manufacturing and availability. Also, 2H 2023 includes a December 31, 2023 start of manufacturing.

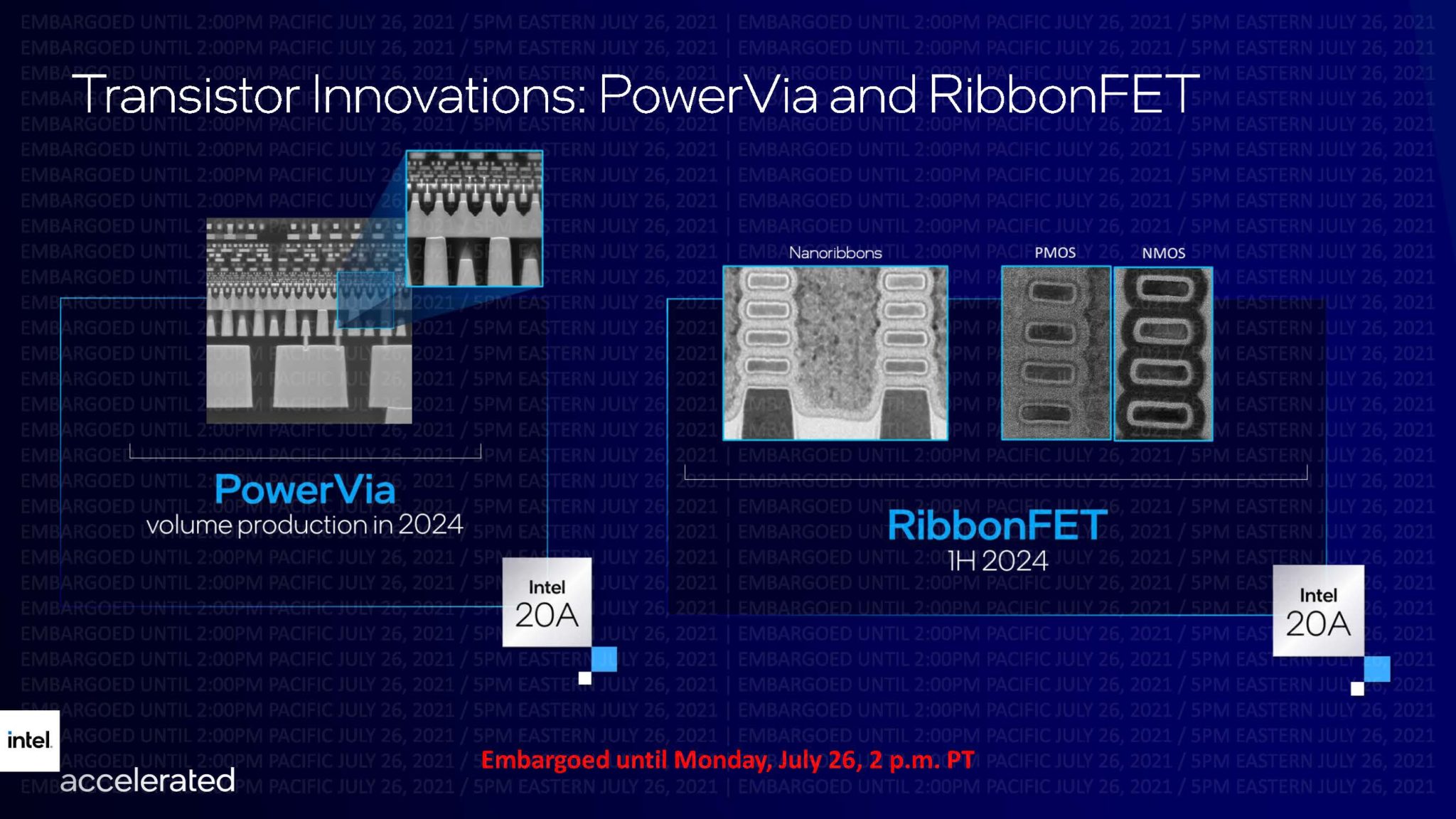

In 2024, Intel will move to Intel 20A. There we get a few new innovations. First is the Intel PowerVia where power is delivered from below by vias thus allowing the top of chips to be used more effectively since power delivery has its own channel. Intel says this will have better resistance/ capacitance while also freeing up more area near the logic gates. On the gates, Intel has a new gate all around technology it is calling the Intel RibbonFET. TSMC is also working on gate all around designs, but this shows where the industry is headed.

Intel Corp. is in the midst of negotiations to construct a U.S.-based “mega-fab” designed to revive American chip production.

Intel CEO Pat Gelsinger said negotiations with local officials are ongoing, and the company expects to announce a U.S. site by the end of the year. Along with necessary foundry infrastructure, including inexpensive power and plentiful water, the chip maker also wants to locate its new fab near a university.

“We need a more resilient but also globally balanced supply chain,” added Gelsinger. Pending legislation providing tax incentives and fund chip R&D would help expand U.S. chip makers’ share of global production from about 12 percent to 30 percent over the next decade as the semiconductor supply chain is reoriented away from Asia, the Intel CEO argued.

https://www.eetimes.com/with-mega-fab-coming-intels-gelsinger-promotes-chip-bill/Its entry into the foundry business includes new customers Amazon Web Services and Qualcomm. AWS will adopt Intel’s packaging technology while Qualcomm will base its smartphone platform on the chip maker’s A20 process node expected to be available in 2024.